In April, the media leaked devastating news. In the state Duma were amendments to the Civil code related to mortgages. It seems nothing special, if not one of the wording – “the loan amount can be returned ahead of schedule only with the consent of the lender”. These lines could dramatically change the lives of millions of borrowers. In fact, they forbid them ahead of time to repay the mortgage. Where did the amendment and will accept it? “KP” was dealing with experts.

To take a long time, to give quick

Mortgage – a sore subject in our country. So much so that a few years ago there was a fantastic book – a “mortgages for fools”. About a family who cannot save for a down payment for a mortgage. And then the newlyweds begin to seduce the new apartment. To get it, they have to give their body after death for medical purposes. Fiction? Yes, but some potential mortgage holders are willing to participate in such a transaction.

– Took a mortgage when was normal operation. Now wages have fallen, and the wife went on maternity leave. She’s due soon, but we at least go to the street. Money to pay the Bank, there is not expected – says Oleg, the reader of “KP” of the suburbs.

There are other stories. Dmitry took the credit before the 2008 crisis and, importantly, in rubles. Then the apartments constantly go up and incomes of borrowers increased. In General, it back the loan ahead of schedule – in five years.

– I from each paycheck set aside more money than needed for the payment. So the whole debt is cleared. Overpaid, not so much. Now sell the apartment, take a loan and buy more, ” says the man.

Mortgage in something like a war. Only financial. And it has deserters (like Dimitri) who had left the front early. To the great relief for myself and grief for the Bank.

The missing amendment

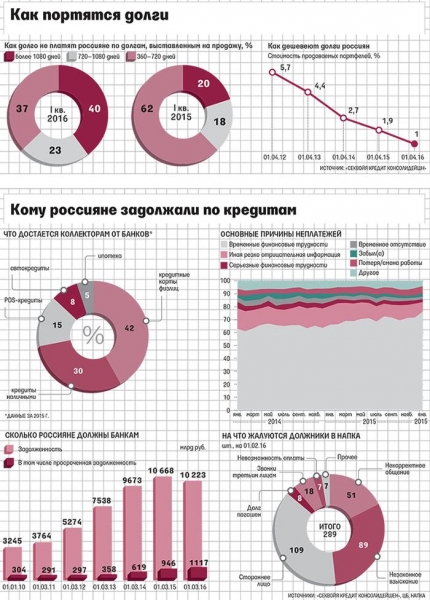

The beauty of the mortgage to the Bank that the income he receives for many years. Yes, and almost no risks – in real estate. But in Russia almost every second Ipotechny pays the debt early.

“Disorder” – decided the financiers. And thinking of the possibility of early redemption to prohibit through amendments to the Civil code. But to do so without noise and dust did not work.

– We do not support this initiative, ” she said the Minister of construction and housing Mikhail Men.

– Due to the crisis and lower incomes limit the rights of mortgage borrowers in a timely manner, is less categorical, expressed the head of the Association of Russian banks Garegin Tosunyan.

– A ban on early repayment – absolutely unacceptable. If approved, these amendments would arise mortgage slavery, – said the Chairman of the Board of the International Confederation of consumer societies Dmitry Yanin.

In General, once it became clear what the response would be if the amendment is not something that is accepted, and even just consider.

Who benefits

In General, a strange thing happened. So was an amendment or not?

– Of course, – told “KP” on the condition of anonymity familiar with the situation the banker. – But when the hype went up, it was quickly hushed up, out of harm’s way.

And make them wanted that’s why. Banks have accumulated an excess of money. And he, most likely, will grow. They need somewhere to invest. The mortgage for this purpose, looks attractive. Rates are 12 – 14% per annum. But inflation is falling. And with it will fall and bet. What will the debtors, which pay higher interest rate? Will refinance the debt (that is, to take a cheaper loan in another Bank).

– The big banks navidale loans at 14 – 15% per annum. Of course, they are beneficial to all people 15 – 20 years to pay them at such rates. If amendments are adopted, they would have been right to not let go of a debtor, that is, there would be mortgage slaves, ” the source explained “KP”.

On freedom with a clear conscience

Than advantageous to repay the loan before the term the borrower? 10 years ago this was not the point: the real estate price rose sharply, inflation was high and wages were rising at a faster pace. Now the situation is the opposite: rates have remained high, but housing is not expensive, salaries are not increasing and inflation will definitely be lower. So now the mortgage is more profitable to give early. In order not to pay the rent twice and three times.

– Well not in a hurry to put out a 25 year mortgage at a rate of 2% per annum and it is very unpleasant to do it at a rate higher than 12%, when the price of the apartment doubled in 7 – 8 years, – said the Director of analytical Department of National rating Agency Karina Artemiev.

– Early repayment is beneficial for the borrower. For example, if it extinguishes the debt by 5 million in 5 years instead of 30, saving 9 million rubles – calculated analyst on Bank ratings “Expert RA” Ivan Uklein.

By the way, in some European countries ban or restrictions on early repayment do exist. But with minimal (and sometimes even negative – see “well, Well!” and “they have”) bets, it’s not so bad for customers.

.

Well, well!

Here you do not Denmark

Hans-Peter Christensen – conventional mortgage the borrower. He lives in Denmark. At the time, he took out a loan and 11 years of faithfully paying the Bank. And this year – what a pleasant surprise – the Bank took it and he gave him his money back. About $40.

How is this possible? In Denmark (as in many Western countries) the loans are mostly issued at floating interest rates. They are formed as follows: the interest rate at which credit institutions borrow money from the local Central Bank, plus the Bank’s profit. Therefore, the floating rate is not a constant value. Recently the national Bank of Denmark has lowered the discount rate. To minus 0.65 percent. As a result, some borrowers percentage was also below zero.

Just do not think that the Danes can now borrow from the Bank, but he still will pay for it. This happened only with those who took a mortgage a long time. And the body of the debt they still owe to pay regularly. Just from this amount, the Bank returns them a fraction of a percent.

– In Europe the situation is phenomenal. But the floating rate is both opportunities and risks for the borrower. At any moment everything can change, and the debtor will pay the mortgage 2 – 3%, and even higher, says Bank expert Dmitry Shapochkin. And in this case, the monthly payment could rise sharply.

And the Bank in any situation is his margin. And he’s always in the black.

THEY HAVE

Credit cheaper rent

Patrick lives in France. He is 32 years old. He – the seller-consultant in the auto center. A few years ago, he applied for a mortgage and was satisfied. The loan rate is 2.2% per year.

– To rent an apartment, especially in the capital region, is expensive, ” he says. – Much cheaper to buy a real estate loan.

But there are nuances. We still have to pay for the notarial support of the transaction (2% of the loan amount) and insurance (plus 0,2 – 0,3% to the rate).

In Spain, the more expensive mortgage: fixed rate – 5 – 7%, floating – 3,5 – 4,8%.

– Another opportunity to purchase a house just yet – said “KP” resident of Madrid Enrique de Santiago. – But, of course, want to pay. When took the credit, provided the procedure for early repayment.

In Spain it has limitations. For example, at each additional payment to the Bank you have to pay a Commission up to 1% of the amount. Plus there is a ceiling on the maximum maturity for once. All this needs to be discussed when signing the contract.